“There is no reason in logic or principle to exclude statutory debts from the compass of provisions such as s 553C” as quoted in Smith v Boné (2015) FCA 319 (at 418) was relied upon in Stone v Melrose Cranes & Rigging Pty Ltd [2018] FCA 530 (at 282) although it appears to have its origins in Re ACN 007 537 000 Pty Ltd (in liq); Ex Parte Parker (1997) 80 FCR 1 (“Parker”). That is a bold assertion. Especially if the “statutory debt” is a voidable transaction recovery.

Melrose Cranes, a voidable transaction recovery, leans on Smith v Boné, a misfeasance proceeding for insolvent trading, which in turn leans on Parker, also an insolvent trading recovery, which in turn relied inter alia on the judgment of the High Court in Gye v McIntyre [1991] HCA 60, a bankruptcy case dealing with the question of whether set-off of an unliquidated damages claim should be allowed. The origins of the bold assertion were not born out of a contest involving a statutory voidable transaction recovery.

Also significant is that most of these judgments refer to an absence of detailed submissions on the subject.

In terms of the policy question, there are two competing insolvency regime fundamentals – pari passu and the right of set-off.

Both the voidable transaction regime and the right of set-off are exceptions or modifications to the primacy of the pari passu regime.

But which of the two should prevail? The Courts have focused on the legal interpretation of the wording of Section 553C of the Corporations Act 2001 or Section 86 of the Bankruptcy Act 1966 and have not really considered the effect in relation to other creditors. After all, each of those “statutory debts” referred to in the cases are all recoveries specifically designed to benefit the general body of creditors.

Arguably the right of set-off disturbs the pari passu rule because it allows the creditor to be exposed to the debtor for its net position only. On the other hand, the voidable transaction regime is specifically targeted to achieve pari passu (albeit on the inevitable proviso of insolvency and subject to statutory time limits).

It seems all too easy to get distracted by the fairness and justice as between the relevant parties at the expense of the fairness and justice for the general body of creditors (the raison d’etre of pari passu). I respectfully suggest that common sense, logic, fairness and justice all dictate that the pari passu principle by way of allowing full recovery of the voidable transaction should prevail. The creditor should have the benefit of any set-off entitlement when the court was considering and calculating the impugned transaction(s) e.g. when calculating a running account balance.

Contrary to the bold assertion in Smith v Boné, logic does not favour allowing set-off against the recovery of the voidable transaction.

Highlighting the absence of logic is the curious outcome that the creditors who fare best happen to be the ones receiving precisely half of what they are owed in the six month relation back period.

Examples

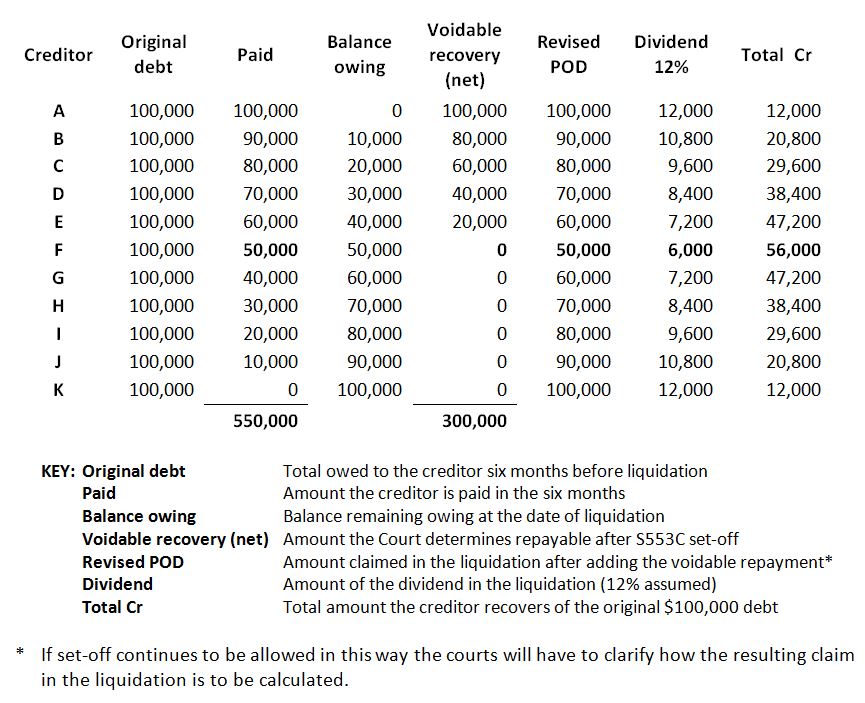

Consider 10 different creditors who are each owed $100,000 going into the relation back period. During the six months creditor A receives payment of its entire debt, creditor B receives payment of $90,000, creditor C $80,000 and so on, so that creditor K receives no payment towards its debt.

For simplicity, assume the liquidator is successful in recovering all the payments in the relation back period but the creditor has been allowed set-off of their outstanding debt as at the date of liquidation in line with the recent judgments. Also assumed is that the liquidator is able to make a 12% distribution to all creditors.

The creditor who was paid all $100,000 of their debt in the relation back period ends up receiving only $12,000 i.e. the liquidator recovers the whole $100,000 as there is no outstanding debt at the date of liquidation to set-off, and the creditor receives a 12% dividend on the $100,000 debt arising upon the repayment.

The creditor who received no payments in the relation back period also receives $12,000 because they still have their original $100,000 debt at the date of liquidation. No set-off arises as there is no voidable transaction recovery.

On a comparison between those two creditors the bold assertion in Smith v Boné and Melrose Cranes might stand up.

However, when you consider the outcome for the creditors in between those two extremes, logic suggests otherwise.

In the pre set-off era each creditor would repay to the liquidator the full amount they received in the six months resulting in them each having a revised proof of debt comprising the residual amount they had owing at the date of liquidation plus the voidable repayment making a total of $100,000. That means they would each receive $12,000 from the liquidation in repayment of their $100,000 debt. This is the pari passu or pro rata objective of the regime. Of course a higher dividend rate would be applicable in this scenario as there is an additional $250,000 recovered from creditors, but that would be distributed among all the creditors – not just these 10. For simplicity, no change in the dividend rate is assumed.

However, the table below shows the creditor receives a vastly different outcome if set-off is allowed (with the exception creditors A and K who were paid all or nothing of the original $100,000 debt respectively).

The resulting returns to creditors highlight the total undermining of the integrity of the voidable transaction regime and by extension, the pari passu fundamental.

Can anyone explain on what rational basis the creditor who happens to have received payment of 50% of their debt should get four times as much back from this insolvent company as the creditor who had been paid all the debt, or the creditor who had been paid nothing?

Even if some policy argument could withstand critical analysis, allowing set-off against voidable transaction recoveries, clearly fails the logic test.

David Blanchett

11 December 2018